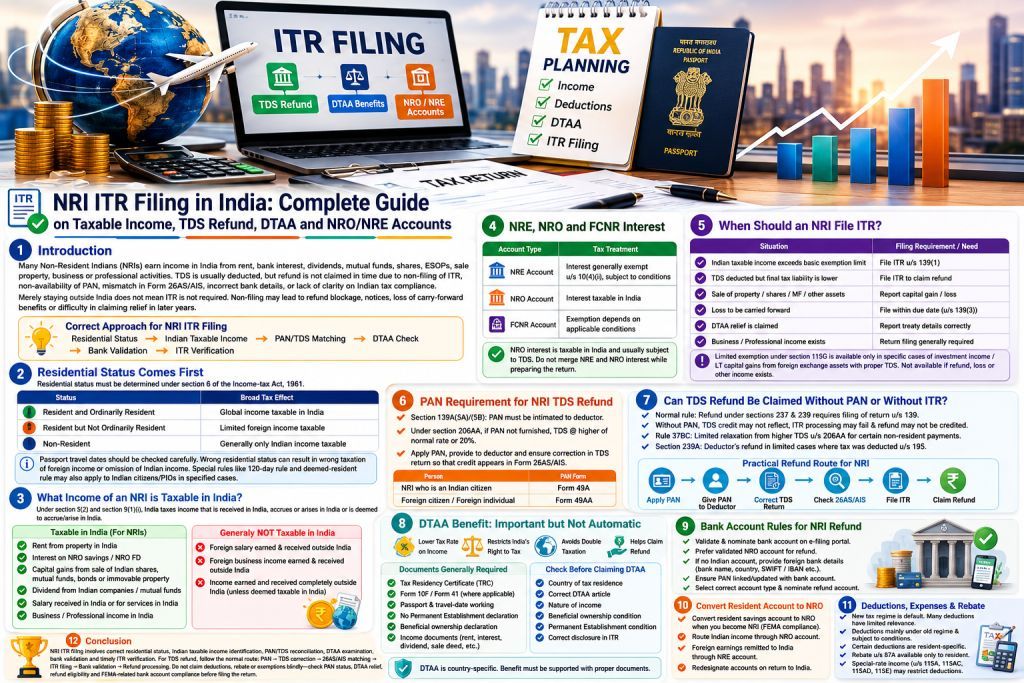

NRI ITR Filing in India: Complete Guide on Taxable Income, TDS Refund, DTAA and NRO/NRE Accounts

1. Introduction

In practice, we have seen many Non-Resident Indians earning income in India from rent, bank interest, dividends, mutual funds, shares, ESOPs, sale of property, business, or professional activities. A common issue faced by many NRIs is that TDS is deducted in India, but the refund is not claimed in time due to non-filing of ITR, non-availability of PAN, mismatch in Form 26AS/AIS, incorrect bank account details, or lack of clarity regarding Indian tax compliance.

Merely staying outside India does not mean that ITR filing is not required. In many cases, non-filing may result in refund blockage, 143(2) scrutiny notices, loss of carry-forward benefits, or difficulty in claiming relief in later years. (You can also learn how AI-based software detects ITR scrutiny to avoid future issues.) This article attempts to cover the practical issues generally faced by NRIs in relation to Indian ITR filing, TDS refund, PAN, DTAA benefit, deductions, and bank account rules.

Residential Status → Indian Taxable Income → PAN/TDS Matching → DTAA Check → Bank Validation → ITR Verification

2. Residential Status Comes First

Before preparing the return, residential status must be determined under section 6 of the Income-tax Act, 1961. A person may be:

| Status | Broad Tax Effect |

|---|---|

| Resident and Ordinarily Resident | Global income taxable in India |

| Resident but Not Ordinarily Resident | Limited foreign income taxable |

| Non-Resident | Generally only Indian income taxable |

For NRI cases, passport travel dates should be checked. Wrong residential status can result in wrong taxation of foreign income or omission of Indian income. Special rules such as the 120-day rule and deemed-resident rule may also apply to Indian citizens/PIOs in specified cases.

3. What Income of an NRI is Taxable in India?

The basic rule is contained in section 5(2). In case of a non-resident, India taxes only income which is:

| Income Type | Taxability |

|---|---|

| Income received or deemed to be received in India | Taxable |

| Income accruing or arising in India | Taxable |

| Income deemed to accrue or arise in India | Taxable |

| Foreign income earned and received outside India | Generally not taxable |

Further, section 9(1)(i) covers income deemed to accrue or arise in India through business connection in India, property in India, asset or source of income in India, or transfer of a capital asset situated in India. Common taxable Indian incomes of NRIs include:

- Rent from property situated in India.

- Interest on NRO savings account or NRO fixed deposits.

- Capital gains from sale of Indian shares, mutual funds, bonds or immovable property.

- Dividend from Indian companies or mutual funds.

- Salary received in India or salary for services rendered in India.

- Business or professional income arising in India.

Foreign salary or foreign business income earned and received outside India is generally not taxable in India merely because the person is an NRI, unless it is received in India or otherwise deemed taxable in India.

4. NRE, NRO and FCNR Interest

Bank interest should be classified carefully.

| Account Type | Tax Treatment |

|---|---|

| NRE Account | Interest generally exempt under section 10(4)(ii), subject to conditions |

| NRO Account | Interest taxable in India |

| FCNR Account | Exemption depends on applicable conditions |

NRO interest is taxable in India and usually subject to TDS. NRE interest and NRO interest should not be merged while preparing the return.

5. When Should an NRI File ITR?

An NRI should generally file ITR in India in the following cases. Ensure you choose the correct ITR form before you start (note that ITR-3 is now available along with ITR-1, 2, and 4 for relevant income types):

| Situation | Filing Requirement / Practical Need |

|---|---|

| Indian taxable income exceeds basic exemption limit | File ITR under section 139(1) |

| TDS deducted but final tax liability is lower | File ITR to claim refund |

| Sale of Indian property, shares, mutual funds or other capital assets | Report capital gain/loss |

| Capital loss or business loss is to be carried forward | File within due date under section 139(3) |

| DTAA relief is claimed | Report treaty details correctly |

| Business/professional income exists | Return filing generally required |

There is a limited exemption under section 115G, where return filing may not be required if the NRI has only specified investment income or long-term capital gains from foreign exchange assets and proper TDS has been deducted. This exemption should not be applied where a refund is to be claimed, loss is to be carried forward, other income exists, DTAA relief is claimed, or TDS mismatch exists.

6. PAN Requirement for NRI TDS Refund

If TDS has been deducted and the NRI wants to claim refund or file ITR, PAN is practically essential. Under section 139A(5A), a person receiving income on which TDS is deductible is required to intimate PAN to the deductor. Under section 139A(5B), the deductor is required to quote PAN in TDS certificates and TDS statements.

Further, under section 206AA, if PAN is not furnished, TDS is generally deductible at the higher of: the rate specified in the relevant provision (always cross-check with the New TDS Rates Chart); the rate in force; or 20%.

If TDS has been deducted without PAN, the NRI should apply for PAN, give PAN to the deductor, and request correction of the TDS return—keeping in mind the TDS return due dates—so that credit appears in Form 26AS/AIS.

| Person | PAN Form |

|---|---|

| NRI who is an Indian citizen | Form 49A |

| Foreign citizen / foreign individual | Form 49AA |

7. Can TDS Refund Be Claimed Without PAN or Without Filing ITR?

As a normal rule, no. Refund is governed by sections 237 and 239. Section 237 provides that refund is available where tax paid exceeds the amount properly chargeable. However, section 239(1) provides that refund claim has to be made by furnishing return under section 139.

Therefore, the normal route for refund is ITR filing. Without PAN, TDS credit may not appear properly, ITR processing may fail, bank validation may fail and refund may not be credited.

Limited relaxation under Rule 37BC

Rule 37BC gives limited relaxation from section 206AA for certain non-resident payments if prescribed details and documents are given to the deductor. It helps in avoiding higher TDS in specified cases, but it does not create a separate refund route without PAN and without ITR.

Apply PAN → Give PAN to deductor → Correct TDS return → Check Form 26AS/AIS → File ITR → Claim refund

7A. Lower/Nil TDS Certificate Before Payment

Where the expected final tax liability of an NRI is lower than the TDS likely to be deducted, the NRI may consider applying for a lower or nil TDS certificate before the payment is made. This is especially useful in cases involving sale of property, rent, interest, capital gains or other Indian income.

| Situation | Practical Benefit |

|---|---|

| Expected tax liability is lower than proposed TDS | Reduces excess TDS deduction |

| Sale of property by NRI | Helps avoid high TDS on gross consideration, where applicable |

| Rent, interest or other Indian income | Helps align TDS with actual tax liability |

| Certificate obtained before payment | Payer can deduct tax at the rate specified in the certificate |

| Certificate not obtained in time | NRI may have to claim excess TDS through ITR refund |

This option is generally examined under section 197 read with Form 13, subject to facts and nature of income. In the event of any payment errors, you can always utilise the online challan correction facility.

8. DTAA Benefit: Important but Not Automatic

DTAA means Double Taxation Avoidance Agreement. It is an agreement between India and another country to avoid double taxation of the same income. In NRI cases, DTAA becomes important because the same income may sometimes be taxed in India as well as in the country where the NRI is tax resident. However, DTAA benefit is not automatic. It must be specifically checked, supported with the right documents, and correctly reported in the ITR.

How DTAA may help an NRI

- It may provide a lower tax rate on certain incomes.

- It may restrict India’s right to tax certain income.

- It may help avoid double taxation by giving credit or relief in the country of residence.

- It may help in claiming refund where excess TDS has been deducted in India.

Documents required for DTAA claim

- Tax Residency Certificate (TRC) from the foreign country.

- Form 10F, where required.

- Form 41, where applicable under the current return/treaty-benefit framework.

- Foreign tax identification number or equivalent details.

- Passport and travel-date working.

- Income documents such as bank interest certificate, dividend statement, rent agreement, sale deed or capital gain statement.

Check residential status → Identify country of tax residence → Check applicable DTAA → Obtain TRC/Form 10F/Form 41 → Compare Act rate and treaty rate → Disclose correctly in ITR → Claim refund, if excess TDS is deducted

9. Bank Account Rules for NRI Refund

For refund, the bank account should be validated and nominated on the income-tax e-filing portal. For NRIs, refund can generally be received in a validated Indian bank account, preferably an NRO account. Where a non-resident does not have an Indian bank account, foreign bank account details may be provided in the ITR (bank name, country, SWIFT code and IBAN).

Before filing, ensure that:

- PAN is correctly linked/updated with the bank account where required.

- Bank account is validated on the e-filing portal (this is critical for faster processing of income tax refunds).

- Correct account type is selected.

- Refund account is nominated.

10. Resident Savings Account Should Be Converted to NRO

A resident savings account should not normally continue as a resident account after the person becomes non-resident under FEMA. When a resident Indian becomes a person resident outside India, the existing resident account should be redesignated as an NRO account.

| Situation | Correct Action |

|---|---|

| Resident becomes NRI | Convert resident savings account into NRO account |

| Indian income such as rent, dividend or interest | Route through NRO account |

| Foreign earnings remitted to India | Generally use NRE account |

| Income-tax refund | Prefer validated NRO account |

| Returning to India permanently | Redesignate accounts as per changed status |

11. Deductions, Expenses and Rebate: Practical Note

Deductions should not be made the main focus of an NRI return because the new tax regime is now the default regime, and many deductions have limited relevance under it. However, where the NRI opts for the old regime or where deduction is otherwise permitted, the following may be checked:

- Salary standard deduction, where salary is taxable in India.

- House property deductions such as municipal taxes, 30% standard deduction and housing loan interest under section 24(b).

- Capital gain deductions such as cost of acquisition, cost of improvement, transfer expenses and eligible reinvestment exemptions under sections 54, 54EC, 54F etc.

- Chapter VI-A deductions such as 80C, 80D, 80E, 80G and 80TTA, mainly under the old regime.

Note: Rebate under section 87A is available only to a resident individual. Therefore, an NRI should not normally claim it.

12. Conclusion

NRI ITR filing is not merely a refund exercise. It requires correct determination of residential status, proper identification of Indian taxable income, PAN/TDS reconciliation, DTAA examination, bank validation and timely ITR verification.

For TDS refund, the normal and correct route is: PAN → TDS correction → Form 26AS/AIS matching → ITR filing → Bank validation → Refund processing.

DTAA should be checked in every important NRI case, especially where there is high TDS, foreign tax residence, Indian capital gains, interest, dividend, royalty, fees for technical services, business income or professional income. Deductors should also align with the quarterly TDS filing schedule to avoid delays in credit for the NRI. Once filed, you can seamlessly track your progress and check your ITR E-Filing status online.