Google Pay Personal Loan in 2026: How to Get Instantly and is it Safe?

Introduction

First of all, if you want to apply for a loan through Google Pay, you must install the application, which most people already have as their go-to UPI app. However, beyond just transferring money or paying bills, Google Pay has now become a powerful gateway for quick credit access.

The question may arise in your mind: How does Google Pay work as a loan interface, and is it RBI-registered?

It is important to understand that Google Pay itself is not a bank or an NBFC (Non-Banking Financial Company). It is just an interface—a middleman. The actual lender is a registered NBFC or Bank (such as DMI Finance, Aditya Birla Capital, L&T Finance, Axis Bank, etc.) with which Google Pay has tied up. The final lender is clearly shown in the last step when the agreement signing page appears, allowing you to check exactly which institution is offering you the loan.

Documents Required

Applying for a digital personal loan is mostly paperless, but you must have your details ready. To apply for a Google Pay personal loan, you need:

- PAN Card (Mandatory for fetching your credit profile)

- Aadhaar Card (For fast DigiLocker KYC)

- Good CIBIL Score (Usually 700+ for the best interest rates)

- Stable Income (Whether salaried or self-employed. If you are salaried, it helps to understand your take-home pay by knowing how employers calculate monthly TDS).

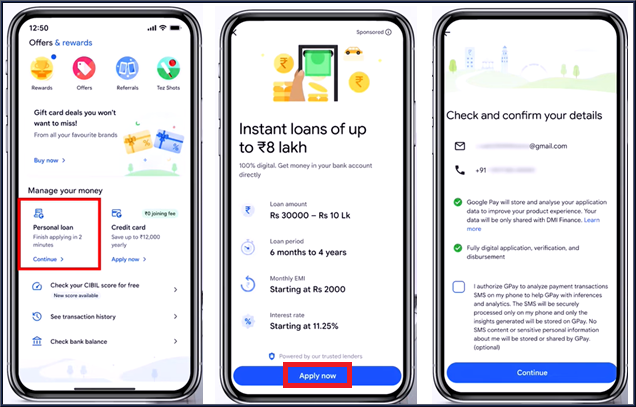

Depending on the partner lender and your creditworthiness, the limits typically range:

• Minimum: ₹30,000

• Maximum: Up to ₹10 Lakh (Note: Certain premium banking partners via GPay can even extend unsecured loans up to ₹50 Lakhs for highly eligible customers).

How to Apply for a Google Pay Personal Loan? (Step-by-Step)

1. Open Google Pay

Scroll down to the "Manage your money" or "Money" section and click on "Loans" or the "Personal Loan" section. Then, tap "Apply Now".

2. Confirm Basic Details

Check and confirm the pre-filled details such as your email ID and mobile number. Tick the consent checkbox and click "Continue".

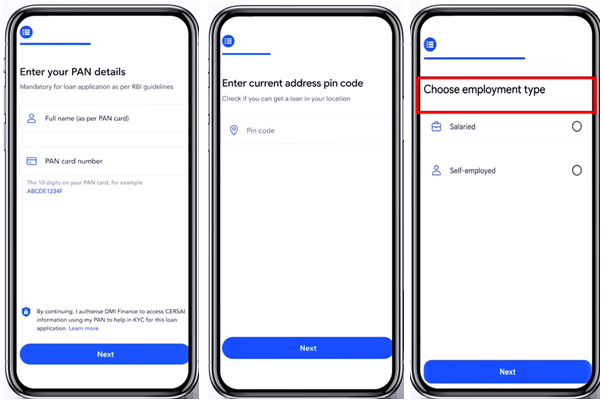

3. Enter Personal Details

You will need to manually provide:

- PAN card details and your exact Date of Birth as per PAN.

- Address PIN code and Residence Type ("Owned" or "Rental") along with the duration you have lived there.

- Employment type (Salaried or Self-Employed) and monthly income.

- Employment details (Company name, total work experience in years, and work address).

Tip: Always ensure your income declaration matches what you report to the Income Tax Department. Major discrepancies between loan applications and ITRs can sometimes trigger automated checks. (Read more about how AI-based software detects ITR scrutiny or what a 143(2) Scrutiny Notice entails).

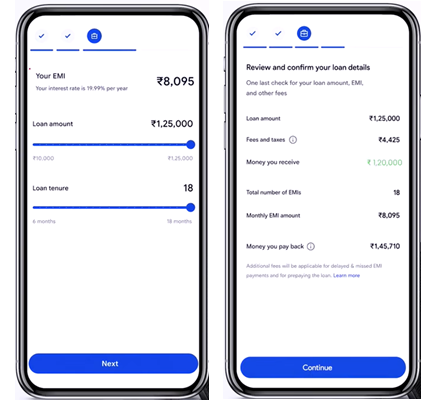

4. Review Loan Offer

Accept the terms & conditions. The platform will then check your PAN and CIBIL score. If approved, you will see a detailed loan offer. Check the approved loan amount, interest rate, processing fee, EMI, and tenure before accepting.

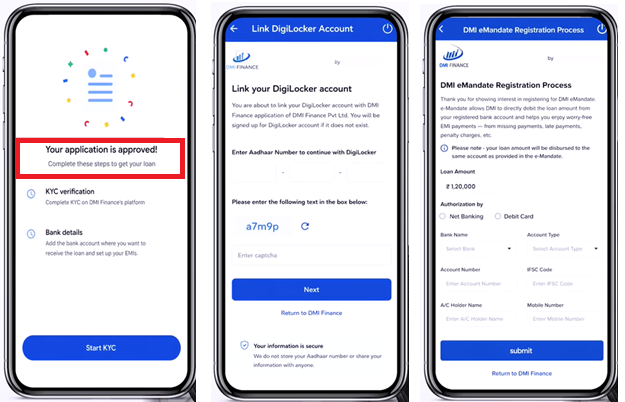

5. Complete KYC and e-Mandate

Once you accept the offer:

- Take a clear selfie and submit it.

- Enter your Aadhaar number to fetch your KYC digitally via DigiLocker.

- Complete the e-mandate registration process. e-Mandate allows the lender (e.g., DMI Finance) to directly auto-debit the EMI from your registered bank account every month. This helps you avoid missing payments, late fees, and penalty charges.

The final summary will display your lender's name, loan amount, and Net EMI. Keep sufficient balance between the 1st and 6th of every month for auto-debit!

How To Check Lender Identification and RBI-Registration?

It is always a safe practice to verify if the NBFC offering you the loan on Google Pay is legally registered with the Reserve Bank of India.

- Once you see the lender's name (e.g., DMI Finance, L&T Finance), go to the official RBI website: www.rbi.org.in.

- On the left side, click on "RBI Regulated Entities" > "Non-Banking Financial Companies".

- Open the NBFC PDF list and search for the exact company name.

Tax Benefits on Personal Loans

A personal loan is a liability that must be repaid, but did you know you can actually claim tax deductions on the interest paid? You can claim these deductions if the personal loan is specifically utilized for:

- Home renovation, construction, or improvement: Interest is deductible under Section 24(b) of the Income Tax Act.

- Business purposes: The interest paid can be claimed as a business expense, reducing your overall taxable business income.

- Higher education: Though usually reserved for strict education loans (Section 80E), if the personal loan is explicitly tracked and used for education, certain exemptions may apply depending on how it's structured.

To claim these tax benefits when filing your ITR, you must retain proper evidence. Keep your loan agreement, annual interest certificate, and proof of end-use (like renovation bills or business invoices). Before filing, make sure to choose the correct ITR form (e.g., ITR-3 for business income).

Also, check your Form 26AS and keep the most important documents for ITR filing handy. If you are expecting a refund after claiming deductions, following proper procedures ensures faster processing of your income tax refund. You can always check your ITR E-Filing status online.

Conclusion

Google Pay personal loans in 2026 have emerged as a highly convenient option for quick, collateral-free funding. Because GPay partners with trusted, RBI-registered lenders, the platform is safe and secure. However, borrowers should always compare pre-approved offers, double-check the actual interest rates (which vary based on your CIBIL profile), and understand all processing fees before accepting.

While digital loans offer instant liquidity, if you have a pre-existing relationship with a traditional bank, consider checking their loan offers first, as they might provide slightly lower interest rates or more flexible repayment terms.