यूनिफाइड पेंशन स्कीम (UPS): पात्रता, लाभ, गणना और पूरी जानकारी

Unified Pension Scheme (UPS)

A Complete Guide for Central & State Government Employees – Eligibility, Calculations, Benefits, NPS vs UPS Comparison, and Latest Notifications.

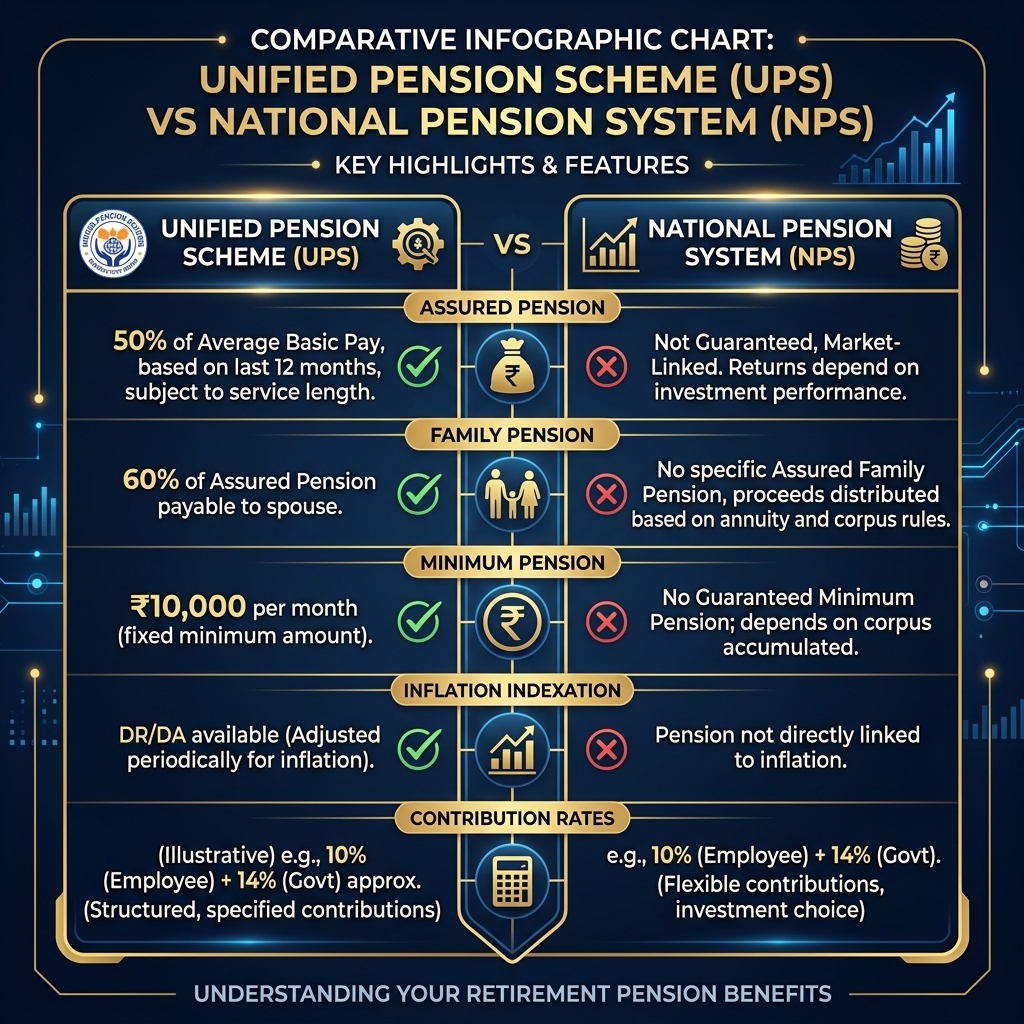

- Assured Pension = 50% of Average Basic Pay (last 12 months)

- Min. Service for full pension = 25 Years (Proportionate for 10-24 yrs)

- Family Pension = 60% of Pensioner's payout

- Minimum Guaranteed Pension = ₹10,000 / month (after 10 yrs service)

- Inflation Protection = Dearness Relief (DR) linked to CPI-IW

- Lumpsum payment on superannuation = 1/10th of (Pay+DA) for every 6 months service

- Matching Govt. Contribution: 18.5% (10% individual + 8.5% pool)

- Past NPS retirees (since 2004) are eligible with interest (PPF rate)

1. What is the Unified Pension Scheme (UPS)?

The Unified Pension Scheme (UPS) is a new pension scheme approved by the Union Cabinet of India, scheduled to become operational on 1st April 2025. It serves as a middle-ground alternative to the Old Pension Scheme (OPS) and the National Pension System (NPS), aimed at addressing government employees' concerns regarding retirement security and pension predictability.

UPS is a 'fund-based' assured payout system. It combines regular monthly contributions from employees and the government with a centralized pooled fund to secure a guaranteed retirement income. Unlike NPS, which is entirely market-linked and lacks pension guarantees, UPS ensures a fixed payout independent of immediate market fluctuations at the time of retirement.

2. The 5 Core Pillars of UPS

The Unified Pension Scheme is anchored on five fundamental pillars designed to provide adequate and inflation-protected retirement benefits:

Superannuating employees will receive a monthly pension equivalent to 50% of the average basic pay drawn during the last 12 months of service.

- Full Assured Pension: Admissible upon completing a minimum of 25 years of qualifying service.

- Proportionate Assured Pension: Admissible for qualifying service ranging between 10 and 24 years, calculated proportionally based on the years of service.

In the unfortunate event of the pensioner's demise, their legally wedded spouse will receive an Assured Family Pension equivalent to 60% of the pension that the employee was receiving or was admissible to receive immediately prior to their demise.

If an employee retires after completing a minimum of 10 years of qualifying service, they are guaranteed an Assured Minimum Pension of ₹10,000 per month. This protects low-income employees and those with shorter career spans, provided contributions were regularly credited and no premature withdrawals were made.

Unlike fixed pension models, the assured pension, family pension, and minimum pension under UPS are fully inflation-indexed. Dearness Relief (DR) will be added to the pension payouts, calculated in the same manner as the Dearness Allowance (DA) provided to active government employees (based on the Consumer Price Index for Industrial Workers - CPI-IW).

Over and above the monthly assured pension, retirees are eligible for a one-time lumpsum payment at retirement. This lumpsum is calculated as:

Lumpsum Payout = (1/10 × Total Emoluments) × L

- Total Emoluments: Basic Pay + Dearness Allowance (DA) as on the date of superannuation.

- L: Number of completed six-monthly periods of service based on contribution months.

- This payment is a purely additional benefit and does not reduce the monthly assured pension.

3. Eligibility Criteria & Retirement Scenarios

The Unified Pension Scheme applies to Central Government employees covered under the NPS who choose this option. It is also designed to be adaptable by State Governments. The pension starts under the following circumstances:

| Retirement Type | Service Requirement | Pension Commencement Date | Admissibility |

|---|---|---|---|

| Superannuation | Min. 10 Years | Immediate (from next day of retirement) | Full pension for 25+ years, proportionate for 10-24 years. Guaranteed min. ₹10,000. |

| Voluntary Retirement (VRS) | Min. 25 Years | Deferred (from date of normal superannuation age) | Full pension based on average pay prior to voluntary retirement. |

| FR 56(j) Retirement | Min. 10 Years | Immediate (from date of compulsory retirement) | Admissible provided it is not a penalty under CCS rules. |

| Resignation/Dismissal/Removal | Any | Not Eligible | UPS options and pension benefits are cancelled. |

4. Contribution Structure: Employee vs Government

The funding mechanism of the Unified Pension Scheme relies on a split contribution model. Here is how individual and pool corpuses are built:

- Employee Contribution: Stays fixed at 10% of (Basic Pay + DA). This is identical to the current NPS employee contribution and is credited directly to the employee's individual corpus.

- Government Matching Contribution: Increased to 10% of (Basic Pay + DA) credited to the individual corpus. Additionally, the government contributes an estimated 8.5% on an aggregate basis to a pooled corpus to cover the risk and guarantee the assured payouts.

- Total Government Contribution: Approximately 18.5% of (Basic Pay + DA).

5. The Concept of "Benchmark Corpus"

Under the UPS, a Benchmark Corpus is computed for each employee by the PFRDA based on default investment options. It represents the value that should have accumulated under standard conditions:

- At superannuation, the value equivalent to the benchmark corpus is transferred to the Government Pooled Pension Fund to secure the monthly Assured Pension.

- If the employee's individual corpus is higher than the benchmark corpus (due to selecting aggressive investment choices that performed well), the employee transfers only the benchmark value and gets to keep the surplus cash.

- If the individual corpus is lower than the benchmark corpus (due to conservative choice performance), the employee can arrange for additional contributions to plug the gap or accept proportionate payouts.

6. 8th CPC Notification: Last Date for Memorandum Submission Extended

Government of India

Eighth Central Pay Commission

No. 16/4/2026-IDM/8CPC | Dated: 29th May, 2026

NOTICE

The last date for submission of Memorandum to Eighth Central Pay commission stands extended to 15.06.2026. This is the final timeline for submission. No further extension shall be granted.

2. The memorandum should only be submitted on the Commission’s website (8cpc.gov.in). Please note that hard copies/physical copies/ emails/pdfs of the memorandum may not be considered by the Commission.

Sd/-

Abhay N Sahay

Deputy Secretary

Eighth Central Pay Commission

- सुनिश्चित पेंशन = आखिरी 12 महीने के औसत बेसिक पे का 50%

- पूर्ण पेंशन हेतु सेवा = न्यूनतम 25 वर्ष (10-24 वर्ष पर आनुपातिक)

- पारिवारिक पेंशन = पेंशनभोगी की पेंशन का 60%

- न्यूनतम गारंटी पेंशन = ₹10,000 प्रति माह (10 वर्ष सेवा के बाद)

- महंगाई राहत (DR) = उपभोक्ता मूल्य सूचकांक (CPI-IW) से संबद्ध

- सेवानिवृत्ति पर एकमुश्त राशि = (मूल वेतन + DA) का 1/10 हिस्सा प्रत्येक 6 माह की सेवा हेतु

- सरकारी योगदान = कुल 18.5% (10% व्यक्तिगत + 8.5% पूल फंड)

- पूर्व NPS सेवानिवृत्त (2004 से) PPF ब्याज दरों के साथ एरियर हेतु पात्र

1. यूनिफ़ाइड पेंशन स्कीम (UPS) क्या है?

यूनिफ़ाइड पेंशन स्कीम (UPS) भारत सरकार की केंद्रीय कैबिनेट द्वारा अनुमोदित एक नई पेंशन योजना है जो 1 अप्रैल 2025 से प्रभावी होगी। यह राष्ट्रीय पेंशन प्रणाली (NPS) के तहत एक विकल्प के रूप में कार्य करेगी। यूपीएस का मुख्य उद्देश्य पुरानी पेंशन योजना (OPS) की निश्चितता और नई पेंशन योजना (NPS) की वित्तीय स्थिरता को मिलाकर कर्मचारियों को एक सुरक्षित और अनुमानित सेवानिवृत्ति जीवन प्रदान करना है।

यह एक 'फंड-आधारित' सुनिश्चित भुगतान प्रणाली है, जिसमें कर्मचारी और नियोक्ता (सरकार) के नियमित मासिक योगदान का निवेश कर एक केंद्रीय पूल बनाया जाता है, जिसके माध्यम से मासिक पेंशन का भुगतान सुनिश्चित किया जाता है। एनपीएस के विपरीत, जहां पेंशन पूरी तरह बाजार के उतार-चढ़ाव पर निर्भर होती है, यूपीएस सेवानिवृत्ति के समय बाजार की स्थिति से परे जाकर एक निश्चित सुनिश्चित पेंशन की गारंटी देती है।

2. यूनिफ़ाइड पेंशन स्कीम (UPS) के 5 मुख्य स्तंभ

यूपीएस सरकारी कर्मचारियों को पर्याप्त और महंगाई-सुरक्षित सेवानिवृत्ति लाभ देने के लिए इन पांच मूलभूत स्तंभों पर आधारित है:

कर्मचारी को उसके सेवानिवृत्त होने से ठीक पहले के अंतिम 12 महीनों के औसत मूल वेतन (Basic Pay) का 50% सुनिश्चित मासिक पेंशन के रूप में मिलेगा।

- पूर्ण सुनिश्चित पेंशन: कम से कम 25 वर्ष की अर्हता सेवा (Qualifying Service) पूरी करने पर मिलेगी।

- आनुपातिक पेंशन: यदि सेवा काल 10 से 24 वर्ष के बीच है, तो सेवा के वर्षों के अनुपात में पेंशन दी जाएगी।

पेंशनभोगी के निधन के मामले में, उसके कानूनी रूप से विवाहित जीवनसाथी को कर्मचारी की मृत्यु से ठीक पहले मिलने वाली सुनिश्चित पेंशन का 60% पारिवारिक पेंशन के रूप में दिया जाएगा।

कम से कम 10 वर्ष की सेवा पूरी करने के बाद सेवानिवृत्ति पर न्यूनतम ₹10,000 प्रति माह पेंशन की गारंटी होगी। यह कम वेतन पाने वाले या छोटी सेवा अवधि वाले कर्मचारियों के लिए एक बड़ी राहत है, बशर्ते उन्होंने समय पर नियमित योगदान दिया हो और कोई प्री-मैच्योर निकासी न की हो।

यूपीएस के तहत मिलने वाली सुनिश्चित पेंशन, पारिवारिक पेंशन और न्यूनतम पेंशन पर महंगाई राहत (Dearness Relief) देय होगी। इस महंगाई राहत की गणना सेवारत कर्मचारियों के महंगाई भत्ते (DA) की तरह ही औद्योगिक श्रमिकों के उपभोक्ता मूल्य सूचकांक (CPI-IW) के आधार पर की जाएगी, जिससे पेंशन का मूल्य सुरक्षित रहेगा।

मासिक पेंशन के अलावा, सेवानिवृत्ति के समय एकमुश्त राशि भी दी जाएगी, जिसका सूत्र इस प्रकार है:

एकमुश्त राशि = (1/10 × कुल परिलब्धियां) × L

- कुल परिलब्धियां: सेवानिवृत्ति की तिथि पर मूल वेतन (Basic Pay) + महंगाई भत्ता (DA)।

- L: सेवा के प्रत्येक पूर्ण छह महीने की अवधि (पेंशन कॉर्पस में योगदान के महीनों के आधार पर)।

- इस भुगतान से कर्मचारी की मासिक सुनिश्चित पेंशन के निर्धारण पर कोई प्रभाव नहीं पड़ेगा।

3. पात्रता मानदंड और सेवानिवृत्ति परिदृश्य

यूपीएस उन सभी केंद्रीय सरकारी कर्मचारियों पर लागू होगी जो एनपीएस के तहत आते हैं और इस विकल्प को चुनते हैं। राज्यों द्वारा अपनाए जाने पर यह राज्य कर्मचारियों पर भी लागू होगी। पात्रता की शर्तें निम्नलिखित तालिका में दी गई हैं:

| सेवानिवृत्ति का प्रकार | न्यूनतम सेवा आवश्यकता | पेंशन शुरू होने की तिथि | स्वीकार्यता नियम |

|---|---|---|---|

| अधिवर्षिता (Superannuation) | न्यूनतम 10 वर्ष | सेवानिवृत्ति के ठीक अगले दिन से | 25+ वर्ष पर पूर्ण पेंशन, 10-24 वर्ष पर आनुपातिक। न्यूनतम ₹10,000 की गारंटी। |

| स्वैच्छिक सेवानिवृत्ति (VRS) | न्यूनतम 25 वर्ष | सामान्य अधिवर्षिता आयु पूरी होने की तिथि से | स्वैच्छिक सेवानिवृत्ति से ठीक पहले के वेतन के आधार पर पूरी पेंशन। |

| FR 56(j) के तहत सेवानिवृत्ति | न्यूनतम 10 वर्ष | अनिवार्य सेवानिवृत्ति की तिथि से तुरंत | स्वीकार्य, बशर्ते यह किसी अनुशासनात्मक कार्रवाई का हिस्सा न हो। |

| इस्तीफा / बर्खास्तगी / सेवामुक्ति | कोई भी | अपात्र | यूपीएस के तहत पेंशन और एकमुश्त भुगतान के सभी विकल्प समाप्त हो जाते हैं। |

4. योगदान (Contribution) संरचना

यूनिफ़ाइड पेंशन स्कीम के तहत अंशदान संरचना को कर्मचारी और सरकार के बीच विभाजित किया गया है:

- कर्मचारी का योगदान: मूल वेतन + डीए का 10% रहेगा, जो सीधे कर्मचारी के व्यक्तिगत एनपीएस कॉर्पस में जमा होगा।

- सरकार का योगदान: सरकार कर्मचारी के व्यक्तिगत कॉर्पस में 10% का योगदान देगी। इसके अतिरिक्त, पेंशन पूल को सुरक्षित रखने के लिए सरकार 8.5% का अतिरिक्त अंशदान कुल आधार पर पूल फंड में करेगी।

- सरकार का कुल योगदान: लगभग 18.5% (मूल वेतन + डीए का) होगा।

5. "बेंचमार्क कॉर्पस" की अवधारणा

यूपीएस के तहत, सेवानिवृत्ति के समय PFRDA द्वारा निर्धारित एक बेंचमार्क कॉर्पस की गणना की जाती है:

- निश्चित मासिक पेंशन हासिल करने के लिए बेंचमार्क कॉर्पस के बराबर की राशि कर्मचारी के व्यक्तिगत खाते से सरकारी पूल फंड में स्थानांतरित कर दी जाएगी।

- यदि कर्मचारी का कुल व्यक्तिगत कॉर्पस बेंचमार्क कॉर्पस से अधिक है: (बेहतर निवेश विकल्पों के कारण), तो अतिरिक्त राशि कर्मचारी के खाते में ही रहेगी और उसे नकद भुगतान कर दी जाएगी।

- यदि व्यक्तिगत कॉर्पस बेंचमार्क कॉर्पस से कम है: तो कर्मचारी के पास अतिरिक्त योगदान देकर इस अंतर को पाटने या आनुपातिक दर पर पेंशन स्वीकार करने का विकल्प होगा।

6. 8वें वेतन आयोग (8th CPC) अधिसूचना: मेमोरेंडम जमा करने की अंतिम तिथि में वृद्धि

भारत सरकार

आठवां केंद्रीय वेतन आयोग

संख्या 16/4/2026-IDM/8CPC | दिनांक: 29 मई, 2026

सूचना

आठवें केंद्रीय वेतन आयोग को मेमोरेंडम (ज्ञापन) सौंपने की अंतिम तिथि बढ़ाकर 15.06.2026 कर दी गई है। यह ज्ञापन जमा करने की अंतिम समय सीमा है। इसके बाद कोई अतिरिक्त समय विस्तार नहीं दिया जाएगा।

2. मेमोरेंडम केवल आयोग की आधिकारिक वेबसाइट (8cpc.gov.in) पर ही जमा किया जाना चाहिए। कृपया ध्यान दें कि आयोग द्वारा भौतिक प्रतियों (hard copies), ईमेल या पीडीएफ फाइलों के माध्यम से भेजे गए मेमोरेंडम पर विचार नहीं किया जा सकता है।

हस्ता/-

अभय एन सहाय

उप सचिव

आठवां केंद्रीय वेतन आयोग

UPS vs NPS: Key Differences At a Glance

Below is a comparative breakdown showing how the new Unified Pension Scheme (UPS) stands against the existing National Pension System (NPS):

Unified Pension Scheme (UPS) Calculator

Estimate your Assured Pension, Family Pension, Retirement Lumpsum, and Monthly Contributions instantly.

Latest Orders & Circulars for UPS

Search and track the latest official notifications, letters, and gazettes issued by PFRDA, Ministry of Finance (FINMIN), and DOPPW:

| Order Date | Order Number | Department | Subject & Notification Details | Download |

|---|---|---|---|---|

| 06/10/2025 | Circular No: PFRDA/2025/14/SUP-CG-SG/06 | PFRDA | Extension of cut-off date for exercising Option of UPS under NPS by two months upto 30th November 2025: PFRDA Circular | |

| 30/09/2025 | File No. 11/14/2025-PR | FINMIN | Unified Pension Scheme Cut-Off Date Extended by 2 Months: Deadline Extended to November 30, 2025 | |

| 24/09/2025 | Circular No: PFRDA/2025/13/SUP-CG-SG/05 | PFRDA | Central Government employees on Deputation/Foreign service to submit Physical ‘Form A2’ to opt for UPS | |

| 16/09/2025 | Circular No: PFRDA/2025/10/SUP-CG-SG/03 | PFRDA | Physical Submission of UPS Requests to nodal offices till 30.09.2025: PFRDA Circular | |

| 14/09/2025 | Circular No: PFRDA/2025/08/SUP-CG-SG/02 | PFRDA | PFRDA extends One-time option for Central Government employees who joined services on or after 01.04.2025 and up to 31.08.2025 to opt for Unified Pension Scheme | |

| 02/09/2025 | G.S.R. 599(E). | DOPPW | Gazette Notification: CCS Rules 2025 -Implementation of the Unified Pension Scheme under National Pension System | |

| 24/01/2025 | F. No. FX-1/3/2024-PR | FINMIN | Unified Pension Scheme Gazette Notification: Eligibility and Benefits of the Scheme |

Frequently Asked Questions (FAQs) / अक्सर पूछे जाने वाले सवाल

English: NPS is a defined-contribution, market-linked scheme where pension payouts depend entirely on market gains. UPS is a defined-benefit scheme providing an assured, inflation-indexed payout (50% of basic pay) secured by a government-managed pooled fund.

हिन्दी: एनपीएस एक अंशदान-आधारित बाजार से जुड़ी योजना है, जिसमें पेंशन पूरी तरह बाजार के रिटर्न पर निर्भर करती है। यूपीएस एक सुनिश्चित-लाभ योजना है जो सरकारी पूल फंड द्वारा सुरक्षित एक निश्चित, महंगाई-रहित पेंशन (बेसिक पे का 50%) की गारंटी देती है।

English: Yes, a one-time opportunity will be given to switch from UPS back to NPS. This option must be exercised exactly 1 year before superannuation (or 3 months before voluntary retirement). Once this switch is made, it cannot be reversed. If no action is taken, the employee remains under UPS.

हिन्दी: हाँ, यूपीएस से वापस एनपीएस में जाने का केवल एक बार मौका मिलेगा। यह निर्णय सेवानिवृत्ति से ठीक 1 वर्ष पहले (या स्वैच्छिक सेवानिवृत्ति से 3 महीने पहले) लेना होगा। एक बार यह निर्णय लेने के बाद इसे बदला नहीं जा सकेगा। यदि विकल्प नहीं चुना जाता है, तो कर्मचारी यूपीएस में ही बना रहेगा।

English: Yes, the provisions of UPS will apply mutatis mutandis to past retirees of NPS who superannuated before the date of operationalizing (1st April 2025). They will be paid arrears along with interest calculated as per Public Provident Fund (PPF) rates, after adjusting withdrawals and annuities already paid.

हिन्दी: हाँ, 1 अप्रैल 2025 से पहले एनपीएस के तहत सेवानिवृत्त हुए कर्मचारियों पर भी यूपीएस के लाभ समान रूप से लागू होंगे। उन्हें पिछली अवधि के एरियर का भुगतान लोक भविष्य निधि (PPF) की ब्याज दरों के साथ किया जाएगा, जिसमें से पूर्व में की गई निकासी और वार्षिकी का समायोजन किया जाएगा।

English: Yes, Dearness Relief (DR) is available on both the assured pension and family pension. It is worked out and updated twice a year in the exact same manner as Dearness Allowance (DA) applicable to active employees.

हिन्दी: हाँ, सुनिश्चित पेंशन और पारिवारिक पेंशन दोनों पर महंगाई राहत (Dearness Relief) लागू होगी। इसे सेवारत कर्मचारियों के महंगाई भत्ते (DA) की तरह ही साल में दो बार अपडेट किया जाएगा।